The Wall Street Journal published a well thought out article titled Apartment Rent Growth Set to Keep Slowing This Year, which discusses the fading market conditions that once favored apartment landlords – namely, high occupancy and rent growth. Being a commercial real estate insight company, here is Markerr data to inform investors with differentiated insight into the current market conditions mentioned in the article.

Key Takeaways:

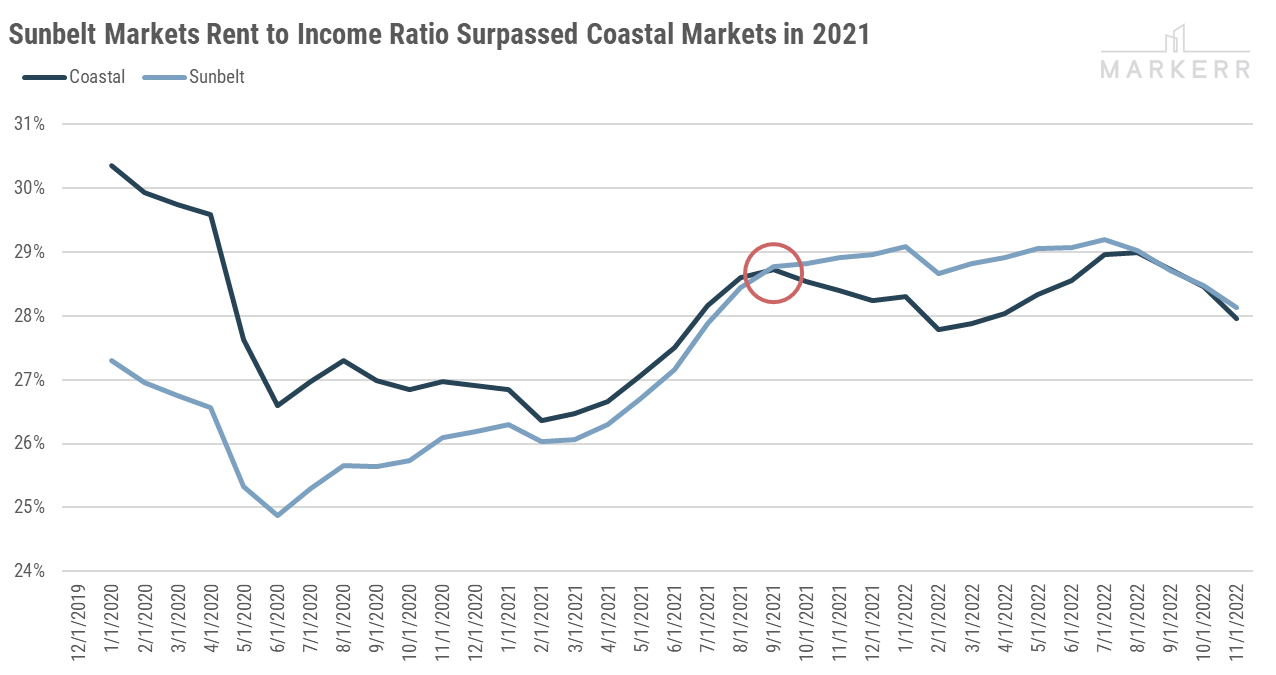

- Sunbelt Markets saw 3rd consecutive month of negative rent growth, but still higher growth than Coastal Markets.

- Sunbelt Markets have become less affordable relative to Coastal Markets using rent to income ratios through November 2022.

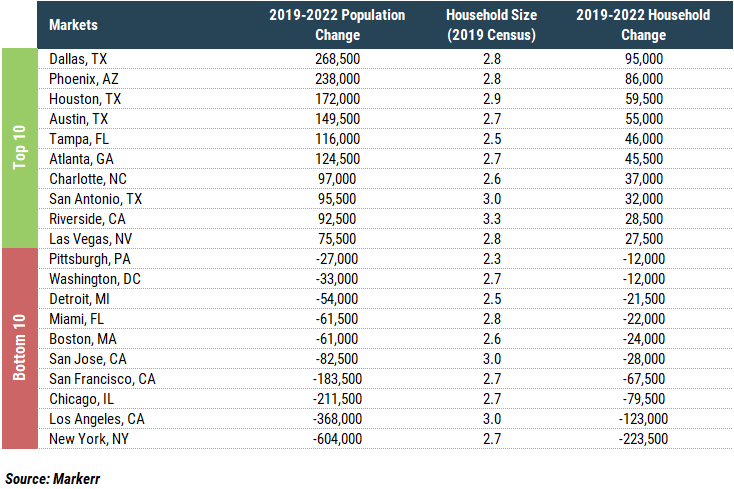

- Coastal Markets saw Out-Migration in the last three years while Sunbelt Markets saw In-Migration.

- Markets in Texas, Carolinas, and Florida rank the highest for Household Formation Growth 2019-2022.

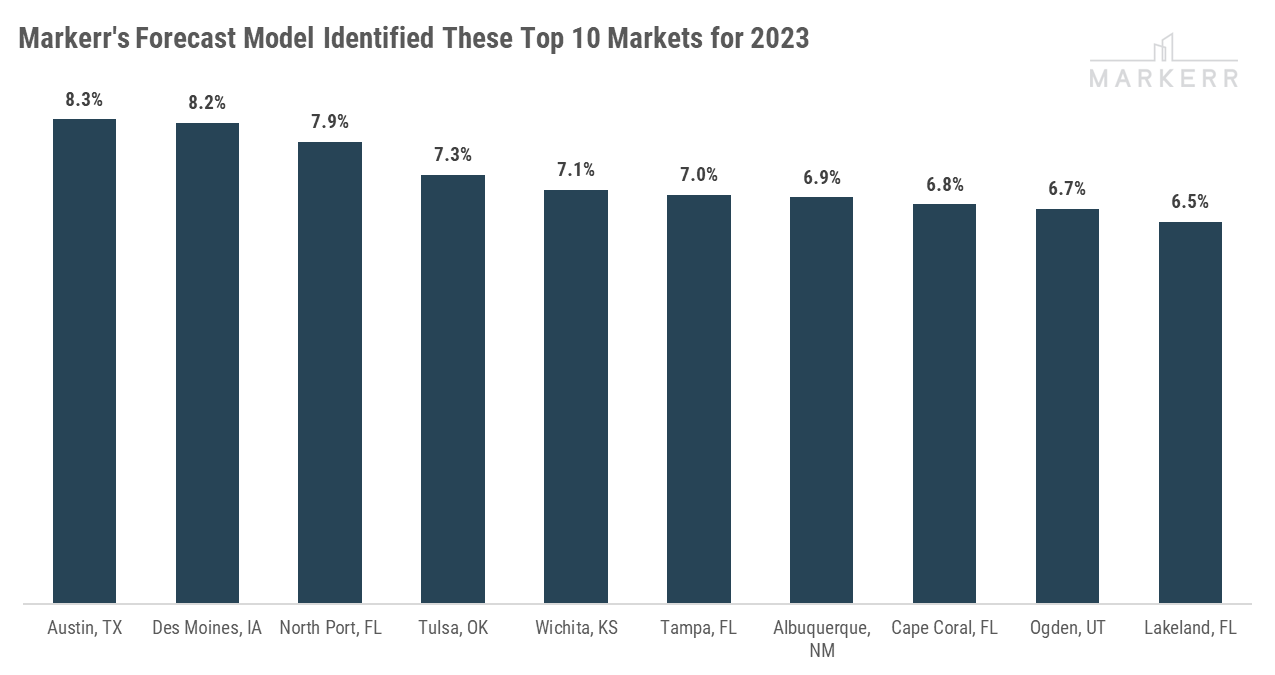

- Markerr forecasts Austin, TX to have the highest rent growth in 2023, followed by Des Moines, IA and North Port, FL.

NOTE: all text in gray italicized fonts are directly quoted from the article.

“Apartment vacancies are piling up. The biggest wave of new rental buildings in nearly four decades is expected to cut the pace of rent growth across the country. Some in-demand Sunbelt cities are already experiencing rent declines, in part because many tenants and people searching for apartments feel they can’t devote any more of their income to rent.”

If supply continues to come online while vacancy rates are increasing, it is expected that the pace of rent growth will decline. Particularly, Sunbelt markets are already experiencing rent declines. Markerr data shows that Sunbelt markets saw their third consecutive month of rent growth decline, however it still outpaces Coastal market rent growth.

“Of the 44 million households that rent, more than 19 million spent 30% or more of their income on rent and other housing costs, according to a December report from the U.S. Census Bureau that estimated spending from 2017 to 2021.”

Markerr data is updated through nearly all of 2022 for both rent and income data, which allows for a real-time tracking of rent to income ratios. The data shows that Sunbelt market’s rent to income ratios surpassed Coastal markets in 2021. However, now in the back half of 2022, the affordability ratios have converged. On average, tenants in both these geographies are spending slightly less than 30% of their income on rent in November 2022.

“In particular, well-paid workers from the Northeast decamped for growing cities in the Sunbelt, where they could work remotely and where their higher incomes commanded more space.”

Markerr Population & Migration data supports this thesis as Coastal markets saw negative out-migration in the last three years, while Sunbelt markets experienced the complete opposite.

“If migration and new household formation continue to slow, analysts said some markets could see a full 12 months of negative rent growth starting sometime this year.”

Citing from an anonymous analyst, the article hypothesizes that if migration and new household formation continue to slow, that some markets could see a full 12 months of negative rent growth in 2023. Markerr provided a table below that shows the top and bottom ten markets that experienced the largest household change in the last three years.

“The coming increase in new apartments is most likely to affect rents at higher-end buildings, because there might not be enough people who make enough money to rent them, according to CoStar.”

An increase of new apartments will certainly impact rents at higher-end buildings since new deliveries are Class A and will compete against other Class A offerings. Markerr provides a unique dataset on the proportion of employees living in every county that earn more than six-figures to help gauge the level of demand for Class A buildings. For investors, having this information will alleviate some concerns surrounding whether there is enough demand for Class A buildings in their respective area.

“Both Yardi and Moody’s expect rents to rise about 3% nationally during the next 12 months, less than half the rate seen in 2022.”

Markerr’s rent forecast leverages a machine-learning approach that allows the model to learn about hidden relationships within components that impacts rent growth. Across the top 100 markets, Markerr forecasts that rent growth will be ~4% in 2023. The forecast does identify markets that will outperform the national average. A full report on Markerr’s latest rent forecast will be released following this article.